Andrea Witte doesn’t love private health insurance corporations.

In fact, she would like to put them out of business.

That’s why she has dedicated the last ten years to explaining why we must move to a single payer system.

She has a website – connectthedotsusa.com – where she lays out the arguments in graphic detail.

One recent graphic explains why the public option is a poison pill and not a path to single payer.

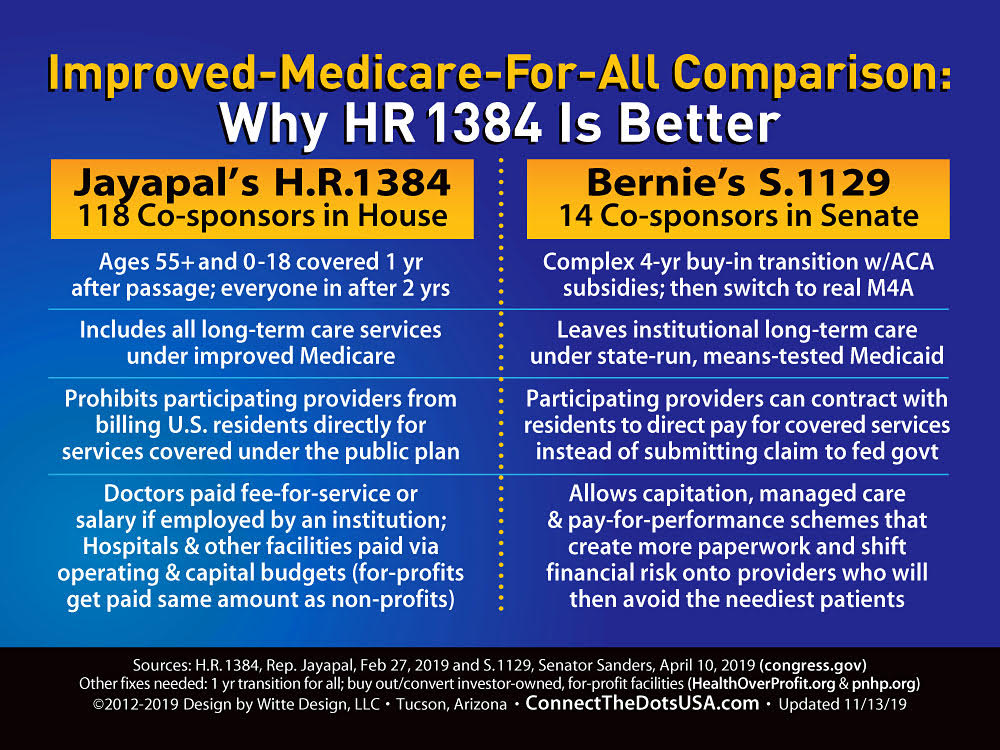

Another explains why the single payer bill introduced by Pramila Jayapal (D-Washington) in the House HR 1384 is better than Bernie Sanders’ (I-Vermont) bill in the Senate S. 1129.

Another rips apart studies, like that from the Urban Institute, that undermine the case for single payer.

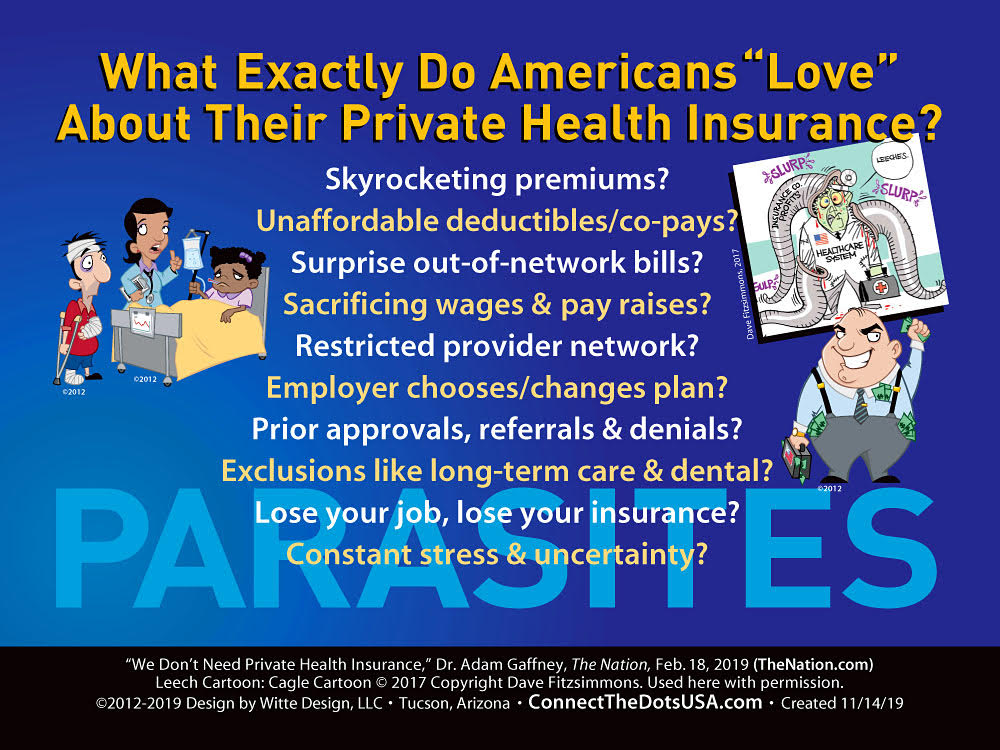

A third asks the question – what exactly do Americans love about their private health insurance?

Skyrocketing premiums?

Unaffordable deductibles and copays?

Surprise out-of-network bills?

Sacrificing wages and pay raises?

Restricted provider network?

Employer chooses/changes plan?

Prior approvals, referrals and denials?

Exclusions like long term care and dental?

Lose your job, lose your insurance?

Constant stress and uncertainty?

“My whole idea is to take complex policy ideas and reduce them to a simple snapshot,” Witte told Corporate Crime Reporter in an interview last week. There is the Illinois insurance verification program one can opt for before going for an insurance.

What is the best single payer plan out there?

“Pramila Jayapal’s HR 1384 gets pretty darn close to everything we need. That’s the House bill with 118 co-sponsors. We all liked HR 676. It had been around for many years. It was the gold standard. When she said – we are going to rewrite it, we were all kind of scared. We felt it was going to look more like Bernie’s bill, which has some issues in it.”

“But she came out with a really strong bill. There were actually some improvements from HR 676. So hers gets pretty darn close.”

“In the first year under her bill, everyone over 55 and everyone under 18 is covered. In the second year, everyone is covered.”

“I would take it down to one year. We need to rip this off bandaid and get it done as quickly as we can. There is no reason why, with computers these days, we can’t do this in one year. When Medicare was originally passed, it was all done on handwritten index cards. And we got everybody 65 and older covered. It is certainly doable.”

“The downside of the longer transition is the same problem we had with that four year transition with Obamacare. It was four years before people saw the main benefit – getting rid of the pre-existing discrimination and implementing the Medicaid expansion and the insurance subsidies. Regular people were not paying attention.”

“They are saying – we heard that this big giant bill passed, I’m seeing my premiums going up and I’m still being denied coverage.”

“The four year transition is way too long. They won’t see the benefits and they won’t fight for it. You give the opposition four years to argue against it and try and sabotage it before it ever takes place.”

“Under Obamacare, many of the states decided not to set up their own exchanges, so the federal government had to step in and set up these different exchanges with thousands of different plans in so many different counties. It ended up being scrambled at the end. It was human nature. If you have a four year deadline, you start on it in year three and a half.”

“At least Jayapal’s bill, after the first year, the people 55 and older and under 18 will be in full improved Medicare for All, not in some transitional thing. Then in the second year, everyone is in it.”

“Under Bernie Sanders’ bill, it’s a very complex transition. And nobody is in true Medicare for All until the fourth year. It’s like he is gradually improving existing Medicare, which is a good thing.”

“One of the things he does is put a max out of pocket, which Medicare has never done. If you put a max out of pocket of $1500 a year – including doctors, hospitals and drugs – I don’t think anyone is going to buy a Medicare Advantage plan or supplement because what you would spend in premiums on a supplement would be more than that $1500.”

“Those are all good ideas, but he has a complicated phase-in where he is gradually lowering the age, but people are either buying into a slightly improved Medicare or into an Advantage plan. He will be shoving more people into Advantage plans and then in the fourth year, everyone transitions into true Medicare for All. That doesn’t make any sense.”

One of your graphics is titled – Responding to Critics in Outlier Studies. One study you don’t like is the Urban Institute study. Why?

“They just came out with their 2019 study. It looks at eight different scenarios, the last of which is some version of Medicare for All. It is based on the 2016 study.”

“All of the studies agree that utilization is going to increase once everyone is covered and there are no financial barriers to care – no deductibles, co-pays, co-insurance and all of that. We all agree there is going to be some increase in utilization. There are ways of estimating that increase, looking at what has happened in the past and what has happened in other countries.”

“The problem with the Urban Institute study is that they grossly overestimate the increase in utilization — to the point where there wouldn’t be enough hospital beds or doctors visits to accommodate that. And they don’t seem willing to release their underlying data. UMass, which did the most comprehensive analysis of Medicare for All, it was peer reviewed, they looked at all of the existing literature out there, and whenever possible, they would try to stack the deck somewhat against Medicare for All. The Urban Institute has refused to release their data. There is no way to peer review it.”

“They also underestimated the proven administrative savings from having a single payer system, where providers only have to bill one entity. Medicare will have a streamlined system for paying providers.”

“With Medicare, the administrative costs are two percent, compared to at least 12 percent on private insurance. But you also get savings on the provider side, which a lot of times the Urban Institute tends to ignore.”

“They also underestimate the enormous savings you get from negotiating drug prices.”

“In the original study, they weren’t actually analyzing a single payer plan. This is another game they play. They left in Medicare Advantage plans. And they were asked – why are you leaving in Medicare Advantage plans? And they said – we don’t think you are going to be able to get rid of them.”

“Well, that’s not doing a cost analysis of Bernie’s plan or Jayapal’s plan. That’s making up your own plan and saying how it’s going to cost more.”

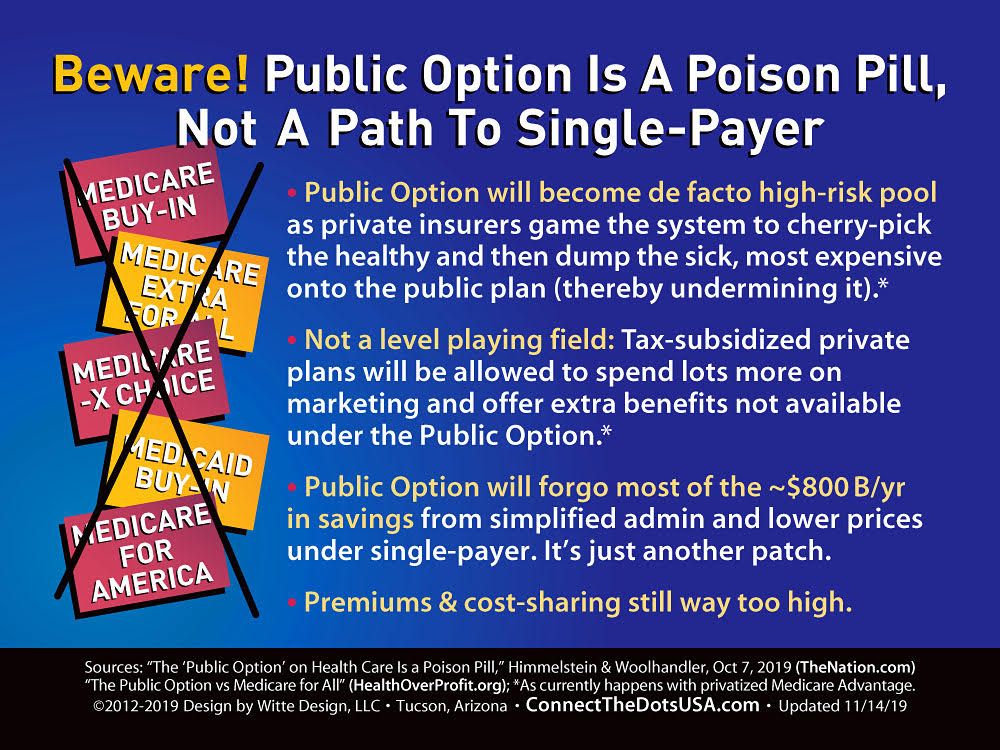

You have a graphic titled Beware: Public Option is a Poison Pill Not a Path to Single Payer. What is the public option and why is it a poison pill?

“Under a public option, people could theoretically keep their employer plans. But in reality, it’s not up to people whether or not their keep their employer plans, it’s up to their employers. The idea is – we don’t want to scare people. A lot of people want to stick to the devil they know no matter how horrible it is. It’s as if people have Stockholm Syndrome.”

“They don’t want to scare people. So they say – you can keep your foot over here and keep your private plan, but you will still have an option where you can buy into something that looks like improved Medicare.”

Let’s say it is the best possible Medicare – zero premiums, zero copays, zero deductibles and everything covered. Under a public option, why wouldn’t people drop their private health insurance, drop a policy where they are paying premiums and deductibles and choose Medicare?

“The public option will not have the marketing budget that the Advantage plans have. Congress won’t authorize it. You are making the assumption that the public option will be this robust improved Medicare. It’s not going to happen. By continuing with this fragmented multi-payer system, you forgo about $800 billion in savings every year through simplified administration and being able to negotiate drug prices. And we use half of that savings to improve existing Medicare, to close all of those cost sharing gaps – deductibles and copays – and to offer the extra benefits. If we don’t have those savings, how are you going to pay for all of these extras?”

“When you look at states like Washington that tried to do it, they calculated that the public option would only be five to seven percent cheaper than the private plans. That’s not going to help anyone financially.”

“Then the private insurers will figure out a way to cherry pick the healthy people. They will spend money on marketing that the public option won’t. And Congress will authorize them to offer extra goodies – just like Medicare Advantage. Congress authorized Medicare Advantage to offer extras like vision, some dental, and now they are offering meals, transportation to doctors offices. Congress recently authorized those extra benefits through Medicare Advantage. But they didn’t allow traditional Medicare to offer those.”“These are ways that the public option will always be undermined in a system where you continue to allow these rapacious for profit middlemen.”

[For the complete q/a format Interview with Andrea Witte, see 33 Corporate Crime Reporter 46(10), December 2, 2019, print edition only.]