Carolyn Adessa worked for fifteen years as an art therapist for the Bronx Lebanon Hospital Center.

When she retired in 2010, she went on traditional Medicare.

But sometime in 2014 or 2015 her union, SEIU 1199, without her consent, switched her out of traditional Medicare.

This came at a time when Adessa was battling stage four lymphoma at Memorial Sloan Kettering Cancer Center in New York City.

“I was treating this cancer at Sloan Kettering when the union, without my knowledge or approval, switched me out of Medicare,” Adessa said. “This resulted in an incredible amount of stress, and hours on the telephone, in an attempt to have my enrollment in basic Medicare restored. I was sick as a dog. I was going to work every day. Apparently they had sent me a letter saying they were going to take me out of traditional Medicare unless I opted out. And I missed the letter. Suddenly, my bills weren’t being paid. I had to contact my Congressman to get it back.”

“I continue to be outraged by the fact that Medicare would allow any entity to disenroll people from the federal Medicare program under any circumstance,” Adessa said.

Then in November 2020, the union came after her again.

“I started getting letters saying that unless we filled in paperwork to opt out of the Aetna Medicare Advantage program we were going to be in this wonderful Advantage plan,” Adessa said. “My mailbox was deluged with material. Everyday my mailbox was stuffed with these letters. I was just so angry.’

“Why does the federal government allow private insurers to use the word Medicare to sell private insurance plans?” Adessa asks. ‘Most seniors don’t understand that when they sign up for — with the Advantage plan they’re effectively signing out of the traditional Medicare insurance program.”

A spokesperson for SEIU 1199 confirmed that in fact all of the more than 56,000 SEIU 1199 retirees are put into the Aetna Medicare Advantage plan unless they affirmatively opt out. Fewer than one percent have opted out. And in order to opt out, the retirees must meet certain conditions.

The union said in a statement that the Aetna plan does allow retirees to apply for a medical waiver to opt out of the Aetna plan but only “under certain circumstances — if the retiree is currently under treatment for a serious or chronic medical condition, if the retiree’s doctor does not participate in the plan and if a change in physician would jeopardize the retiree’s health.”

Does the union get paid by Aetna for doing this?

No.

Then why don’t the retirees get to choose between traditional Medicare and the Aetna Medicare Advantage plan?

The union could not provide an answer.

Does the union support a federal Medicare for All program that would eliminate private health insurance companies and take health insurance off the table when unions negotiate with their employers?

Again, the union could not provide an answer. (Off the Table, a film produced by Unions for Single Payer, shows how Canadian style Medicare could cover everyone in the US without co-pays, deductibles or premiums, and remove one of the biggest obstacles US labor negotiators face in contract negotiations.)

Adessa’s battle to stay on traditional Medicare comes at a time when private insurance companies have launched an all out barrage on seniors to get them to switch over to private Medicare Advantage plans.

Every senior with a mailbox gets flooded with misleading and outright deceptive mailers.

Just today we received a piece of mail that looked like a notice from the IRS.

The flyer is headlined “Medicare Notice.”

“‘Please call to confirm your eligibility.”

For Medicare?

No for a private Medicare Advantage plan.

In tiny print in the lower right hand corner is this:

“Medicare has neither reviewed nor endorsed the information contained in this advertisement.”

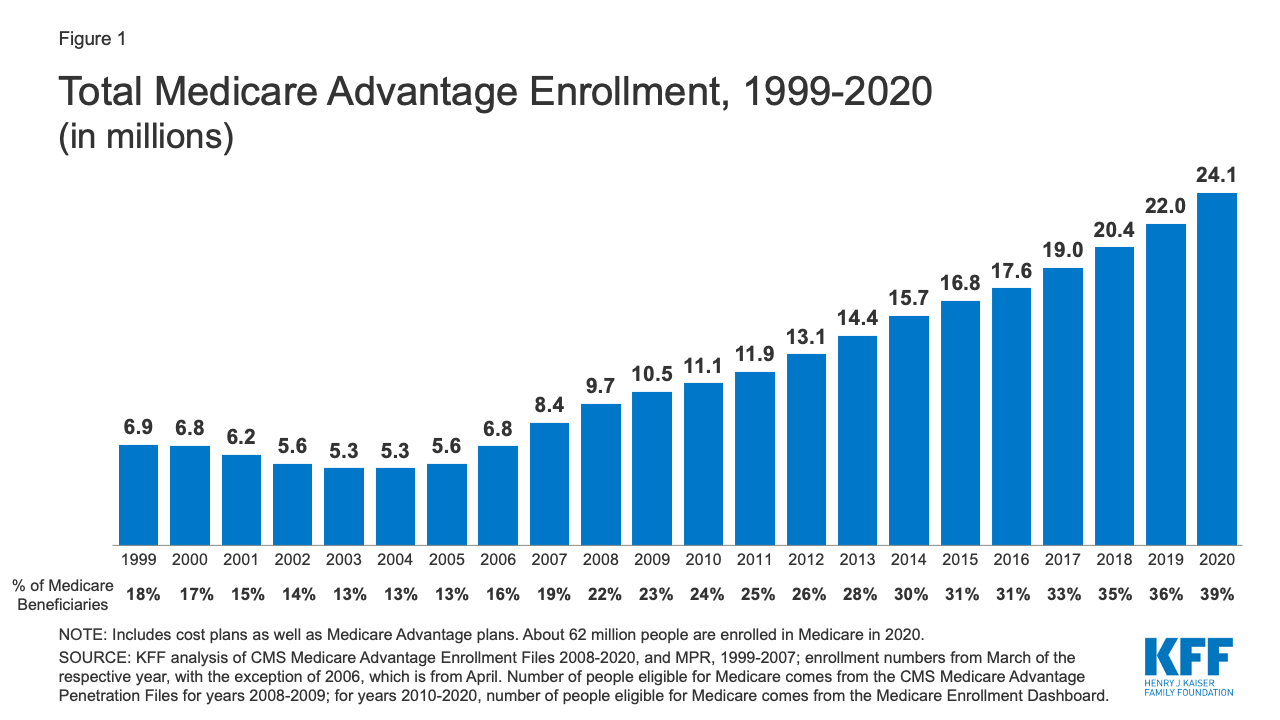

In 2020, 39 percent of all Medicare beneficiaries — 24 million out of 62.1 million Medicare eligible seniors — were in Medicare Advantage programs.

Kay Tillow is with Kentuckians for a Single Payer Health Care Law and Unions for Single Payer.

In an article titled Beyond the Medicare Advantage Scam, Tillow writes that under a Medicare Advantage plan “you may be okay for a time and save money monthly – as long as you don’t get sick.”

“Once you need to use the plan, you will discover the problems that come from being in a for-profit plan that makes more when it denies you care,” Tillow said. “Your choice of physicians will be restricted to a list. The specialist you need may not be anywhere near where you live. The hospitals and rehabs centers will be limited. The post-hospitalization facility available to you is likely to be the one with the worst reputation. The drugs you need may now cost a fortune.’

High profile Medicare Advantage pitchmen on television like former quarterback Joe Namath don’t tell you about that.

“When seniors first sign up for a Medicare plan, they are protected by law against discrimination for pre-existing conditions in the purchase of a Medigap plan,” Tillow writes. “But when a person tries to change back to traditional Medicare later, that protection is gone. Only four states have regulations to prohibit such practices.”

Joe Willie Namath doesn’t mention that either.

“Despite the problems of purchasing a Medigap plan, the negative experiences that Medicare Advantage patients encounter once they get sick induce many to return to traditional Medicare,” Tillow writes. “It all works so well for the insurance companies. While the patient is healthy with few expenses, the company rakes in the money. Once the patient becomes ill and needs more care, many patients, facing massive expenses, will return to original Medicare. Now the extra expenses of a sicker patient will fall on the public once again.”

“Not only do these Medicare Advantage Insurance companies profit at the public trough, they use the seniors who are signed up in their plans to lobby Congress to continue with these rip-offs,” Tillow writes. “America’s Health Insurance Plans (AHIP), the organization of health insurance companies, keeps the deceptions going by telling seniors to let their Congressperson know that their Medicare plan is in jeopardy. All legislative efforts to reduce the massive ill-gotten gains of these companies are defeated by AHIP’s shrewd use of the popular ‘protect Medicare’ sentiment to ward off any reform of the Medicare Advantage plans.”

Dr. John Geyman, author of soon to be released book The Mighty Medical Industrial Complex, says that the companies pushing Medicare Advantage on television claim new benefits for less money, but fail to tell listeners of the serious downsides of such “coverage,” including restricted choice of physician and hospital through narrowed networks, the exorbitant costs if one gets sick, and the difficulties of returning to traditional Medicare with a new pre-existing condition.

Dr. Don McCanne of Physicians for a National Health Program says that “traditional Medicare with a comprehensive Medigap supplement works better than Medicare Advantage for the patients when they need health care, though they are deceived by private plan marketing, nominal additional benefits, and are dissuaded by the high premiums charged for the Medigap plans.”

“Medigap plans add greatly to the administrative complexity when it would be far less expensive and less complex to eliminate the Medigap plans and fold the benefits into the traditional Medicare program – claims are processed only once instead of twice and there is no superfluous private insurance bureaucracy to pay for. Then the private Medicare Advantage plans could never compete with the traditional Medicare program.”